The government is offering you $25,000 to upgrade your heating system, and you pay back exactly $25,000.There is no interest, no hidden fees, or extra charges. That’s called the Mass Save HEAT Loan.

If you borrow the full amount and take seven years to pay it back, your monthly payment is around $297. Compare that to a personal loan at 10% interest, where you’d pay $396 per month and hand over $8,000+ in interest charges by the time you’re done.

Most Massachusetts homeowners don’t know this program exists. In fact, only 40,000 people have availed of the mass save heat loan up until recently. The ones who do often get confused by the application process or are disqualified because they missed a requirement.

This guide walks you through exactly what you need to qualify, how the application works, and what happens after you’re approved.

What Is the Mass Save HEAT Loan?

The Mass Save HEAT Loan gives Massachusetts residents access to 0% interest financing for energy efficiency upgrades. You can borrow up to $25,000 with repayment terms up to seven years.

The program covers:

- Heat pump installations (mini-splits, ducted systems, ground-source)

- Heat pump water heaters

- Insulation and air sealing

- Related energy efficiency work

There’s no prepayment penalty. If you want to pay it off early, you can.

The program exists because upfront costs stop most people from making energy-efficient upgrades. A whole-home heat pump system runs $18,000 to $30,000, depending on your house. Not many people have that sitting around.

The MASS SAVE HEAT Loan removes that barrier.

What are the Requirements for Mass Save HEAT Loan in 2026?

Not everyone qualifies. You need to check every box on this list.

- You Must Own the Property

Renters can’t apply. If you own a multi-family home (up to 4 units), you must live in one of the units.

- Your Utility Must Be a Mass Save Sponsor

Check your electric or gas bill. Your provider needs to be one of these:

- Berkshire Gas

- Cape Light Compact

- Eversource

- Liberty Utilities

- National Grid

- Unitil

If your utility isn’t on that list, you don’t have access to the program.

- You Need a Home Energy Assessment

This is mandatory. You can’t skip it.

Mass Save offers free assessments. You schedule online at MassSave.com or call 866-527-7283. An energy specialist visits your home (or does a virtual walkthrough) and evaluates your current heating system, insulation, and air sealing.

At the end, they tell you which upgrades qualify for financing and hand you your Authorization Form. Without that form, you can’t apply for the loan.

- Your Contractor Must Be HPIN-Certified

HPIN stands for Heat Pump Installer Network. Only contractors in this network can complete work under the HEAT Loan program.

This isn’t optional. If you hire someone who’s not certified, your application gets rejected automatically.

When you’re getting quotes, ask for proof of HPIN certification before you sign anything.

- Your Equipment Must Meet 2026 Standards

Here’s where it gets specific.

Your heat pump system must be:

- ENERGY STAR Cold Climate certified

- Listed on the Mass Save Qualified Product List (QPL)

- Using R-32 or R-454B refrigerant (not R410A)

That last part is new for 2026. The EPA phased out R410A refrigerant. Systems using it don’t qualify anymore.

Your contractor should verify equipment eligibility before ordering anything. If they recommend a system that’s not on the QPL, walk away.

How to Apply for 0% Interest Heat Pump Loan MA

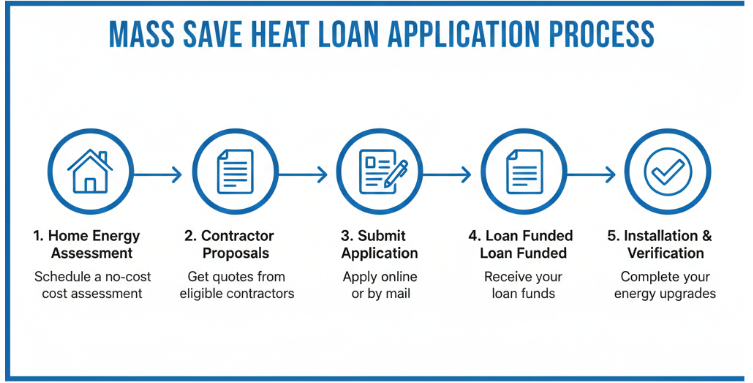

The process takes five steps. You need to complete them in order.

Step 1: Get Your Home Energy Assessment

Schedule your free assessment. The specialist evaluates your home and identifies which upgrades qualify. You walk away with your Authorization Form.

This form expires after a certain period (usually 90-180 days). If you wait too long to apply, you’ll need to do another assessment.

Step 2: Get Written Proposals from Contractors

Talk to at least two HPIN-certified contractors. Get written proposals that include:

- Specific equipment models

- Installation scope

- Total cost

- Contractor’s letterhead

Compare what they’re offering. Equipment matters, but installation quality matters more. A great heat pump installed poorly performs worse than a decent heat pump installed correctly.

Ask how they size systems. The answer should involve a Manual J load calculation, not guesswork based on square footage.

Ask what happens after installation. Do they come back to verify performance? Do they commission the system properly?

Most contractors disappear once the check clears. Find one who doesn’t.

Step 3: Submit Your Application

Take your Authorization Form and signed contractor proposal to a participating lender. The lender reviews your credit and income to determine approval.

Approval typically takes one to two weeks.

Step 4: Get Your Loan Funded

If you’re approved, the lender issues a two-party check made out to you and your contractor. The check gets released after installation is complete, not before.

Step 5: Complete Installation and Verification

Your contractor installs the system. After they’re done, verification confirms the work meets program standards. This might involve submitting photos, invoices, or scheduling an inspection.

Once everything checks out, you endorse the check to your contractor as payment.

Start to finish, expect 4 to 8 weeks.

What are the Reasons for Mass Save Loan Rejection? (And How to Avoid Them)

Applications get denied for specific reasons. Here are the most common.

Using a Non-Certified Contractor

If your contractor isn’t HPIN-certified, your application won’t be reviewed. Verify certification before hiring anyone.

Equipment Not on the QPL

The Qualified Product List updates regularly. Equipment that qualified last year might not qualify now.

In 2026, any system using R410A refrigerant is automatically disqualified. Your contractor needs to recommend equipment with R-32 or R-454B refrigerant.

Debt-to-Income Problems

Even at 0% interest, lenders evaluate whether you can afford the monthly payment based on your existing debt and income.

If one lender denies you, try another. Each has different thresholds.

Expired Authorization Form

Your form has an expiration date. If too much time passes between your assessment and your application, you’ll need to schedule a new assessment.

Missing Weatherization Requirements

For whole-home installations, Mass Save sometimes requires specific insulation and air sealing standards. If your home doesn’t meet them, you need weatherization work first.

The good news is that weatherization also qualifies for HEAT Loan financing.

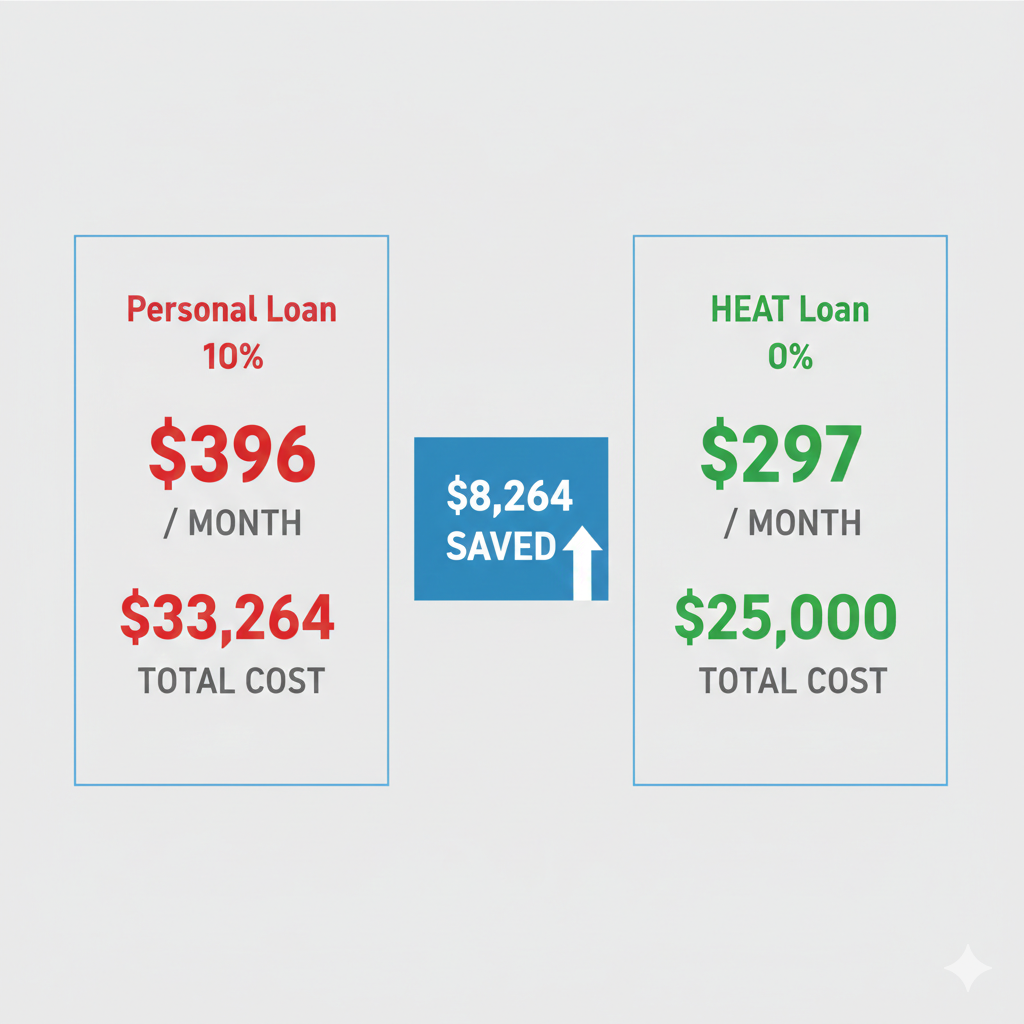

Is Mass Save HEAT Loan Worth It? Let’s Do the Math

Here’s what borrowing $25,000 looks like with different financing options.

| Personal Loan at 10% InterestMonthly payment: $396Total repaid: $33,264Interest paid: $8,264 | Mass Save HEAT Loan at 0% InterestMonthly payment: $297Total repaid: $25,000Interest paid: $0 |

You save $8,264 just by using the HEAT Loan instead of a personal loan.

Add Mass Save rebates on top of that. Depending on your system type and size, rebates can reduce your cost by another $2,500 to $8,500.

What Changed in 2026 in the Heat Pumps Industry in Massachusetts

A few things shifted this year.

- Rebates Decreased

Whole-home rebates dropped from $3,000 per ton (capped at $10,000) to $2,650 per ton (capped at $8,500).

Partial-home rebates went from $1,250 per ton to $1,125 per ton.

The HEAT Loan itself didn’t change. You still get 0% interest for up to $25,000 over seven years.

- No More R410A Refrigerant

Systems using R410A are out. New installations must use R-32 or R-454B refrigerants.

This aligns with EPA regulations phasing out high global warming potential refrigerants.

- Federal Tax Credit Expired

The federal heat pump tax credit (up to $2,000) expired December 31, 2025. Installations in 2026 don’t qualify.

Mass Save rebates and the HEAT Loan still apply.

Questions to Ask Your Heat Pump Contractor Before Signing

Are you HPIN-certified?

Ask for proof. This ensures they can work within the Mass Save program.

Is the equipment you’re recommending on the current QPL?

They should reference the Qualified Product List and confirm the system uses approved refrigerant.

Do you handle the HEAT Loan paperwork?

Some contractors manage everything. Others expect you to handle forms yourself.

What happens if the heating system doesn’t perform as expected?

This is the question most people don’t ask until it’s too late.

Warranties cover equipment failure. They don’t cover a house that’s still cold, or electric bills that don’t match projections, or rooms that never get warm enough.

At VivaVolt, we stay involved until the system performs the way it should. We commission properly. We check airflow in every room. We verify temperatures. We come back when it’s actually cold to make sure what we promised is what you’re getting.

That approach costs us some deals. People who just want the cheapest quote go elsewhere.

But we’re not in the business of selling equipment. We’re in the business of taking responsibility for outcomes.

Do you perform Manual J load calculations?

Proper system sizing requires a Manual J calculation. This determines your home’s actual heating and cooling load.

Oversized systems short-cycle and waste energy. Undersized systems can’t keep up on the coldest days.

If a contractor sizes your system based on square footage alone, they’re guessing.

What Happens After Installation of a Heat Pump

Installation alone doesn’t guarantee performance.

Commissioning verifies the system operates correctly. This includes:

- Checking refrigerant charge

- Verifying airflow in each zone

- Testing defrost cycle operation

- Confirming thermostat programming

- Measuring temperature output

Some contractors include commissioning. Many don’t.

Performance issues usually show up during the first winter. If your contractor doesn’t follow up, you’re on your own to figure out what’s wrong, so choose wisely when it comes to contractors.

Common Questions About the HEAT Loan

Can I use the HEAT Loan with rebates?

Yes. The loan covers installation cost. Rebates reduce your out-of-pocket expense. You apply for rebates separately after installation.

Can I pay off the loan early?

Yes. There’s no prepayment penalty.

What if I sell my home before the loan is repaid?

The loan is tied to you, not the property. If you sell, you pay off the remaining balance.

Do I need perfect credit?

No. Lenders review credit and income, but standards vary. Some homeowners with imperfect credit still qualify.

Why Heat Pumps Work in Massachusetts

People worry whether heat pumps can handle cold weather.

Modern cold-climate heat pumps operate efficiently down to negative 15 degrees Fahrenheit. The systems on the Mass Save QPL are specifically rated for cold climates.

But system performance depends on proper sizing and installation.

An undersized system struggles on the coldest days. An oversized system cycles too frequently, reducing efficiency and comfort.

The equipment is capable. The installation determines whether it performs.

Final Thoughts

The Mass Save HEAT Loan is one of the best financing programs available for Massachusetts homeowners. Zero percent interest with upto $25,000. No prepayment penalty.

But you need to follow the rules: complete the assessment, hire a certified contractor, choose equipment from the QPL, and submit your application before your Authorization Form expires.

When you’re choosing a contractor, look for someone who prioritizes proper sizing, commissioning, and post-install follow-up.

The quality of installation directly impacts whether your system performs the way it should.

At VivaVolt, we approach homes as systems, not products. We don’t just ask “can this be installed?” We ask, “Will this actually work for how this family lives, and will it still make sense years from now?”

If something doesn’t perform the way it should, we don’t hide behind warranties. We stay involved until it does.

That’s the difference between selling equipment and taking responsibility for outcomes.